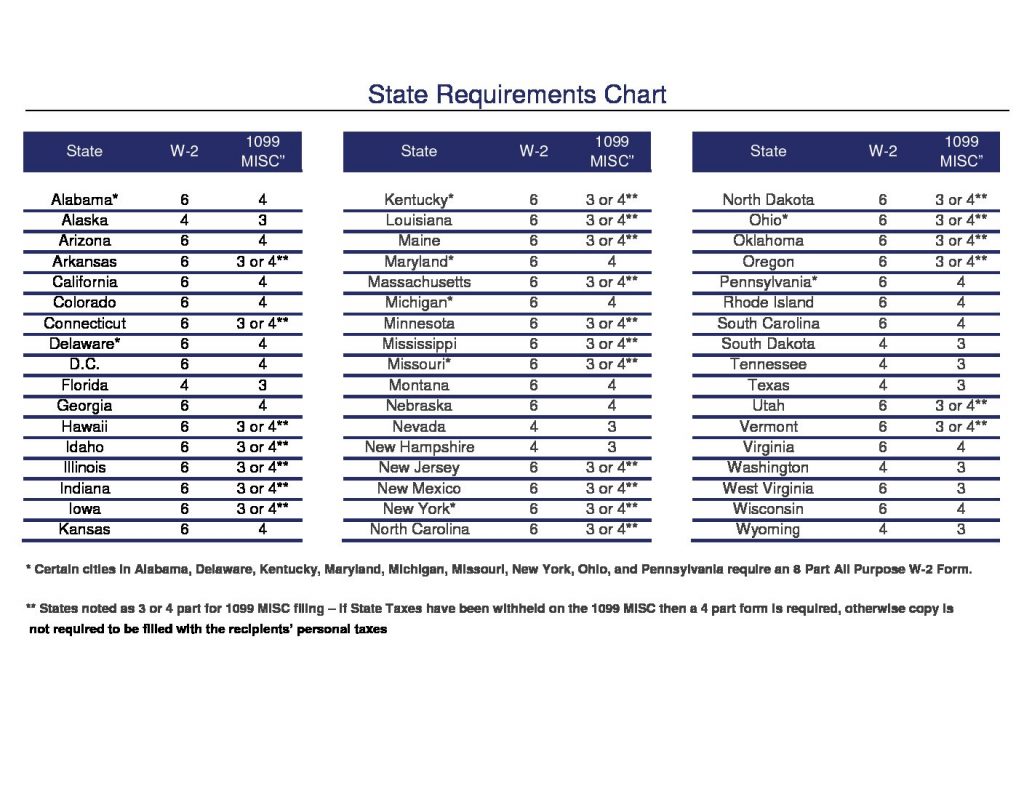

The Tax Cuts and Jobs Act of 2017 (TCJA) increased depreciation limits for passenger vehicles (not SUVs). If the taxpayer doesn’t claim bonus depreciation, the greatest allowable depreciation deduction is:

$10,000 for the first year,

$16,000 for the second year,

$9,600 for the third year, and

$5,760 for each later taxable year in the recovery period.

If a taxpayer claims 100% bonus depreciation, the greatest allowable depreciation deduction is $18,000 for the first year and the same as above for later years.

If you would like to review your deductions and tax planning options we would love to assist you!

The Internal Revenue Service reminds taxpayers who can’t pay the full amount of federal taxes they owe that they should file their tax return on time and pay as much as possible. This will help reduce penalties and interest. If they can’t pay it all, they have some other options.

Options for Paying Now The IRS offers several convenient ways for taxpayers to pay their taxes.

IRS Direct Pay, a free and secure way for individual taxpayers to pay tax bills and make estimated tax payments directly from their bank accounts. The IRS will give taxpayers instant confirmation when they submit their payment.

Taxpayers who use Direct Pay and EFTPS can sign up to get email notifications about their electronic payments. Once taxpayers sign up, they’ll receive email messages that show payments that are scheduled, canceled, returned and modified. They’ll also receive reminders for scheduled payments and confirmation of an address change.

For Direct Pay, taxpayers need to sign up for email updates each time they make a payment. For EFTPS, taxpayers need only sign up for email once to receive the messages each time they pay. Taxpayers can cancel at any time.

The IRS continues to remind taxpayers to watch out for email schemes. Taxpayers will only receive an email from Direct Pay or EFTPS if they’ve requested the email service.

Electronic Funds Withdrawal is an integrated e-file/e-pay option offered only when taxpayers e-file their federal taxes using tax preparation software or through a tax professional. Taxpayers can submit one or more direct debit payment requests from their designated bank account.

Same-Day Wire Transfer. Taxpayers may be able to do a same-day wire transfer from their financial institution. They should contact their financial Institution for availability, cost and cut-off times.

Debit or Credit Card. Taxpayers can pay online, by phone or mobile device if they e-file, paper file or are responding to a bill or notice. It’s safe and secure. The IRS uses standard service providers and business/commercial card networks. Payment processors use taxpayer information solely to process taxpayers’ payments. The payment processor will charge a processing fee.

IRS2Go Mobile App. Taxpayers can get easy access to mobile-friendly payment options including IRS Direct Pay, a free and secure way to pay directly from their bank account, or by debit or credit card using an approved payment processor for a fee. Taxpayers can download IRS2Go from Google Play, the Apple App Store or Amazon for free.

Cash at a Retail Partner. For taxpayers who prefer to pay their taxes in cash, the IRS offers a way for them to pay at a participating retail store. It generally takes five to seven business days to process these payments, so taxpayers should plan to make sure their payments post on time. Publication 5250 contains printable instructions and taxpayers can also go to IRS.gov/paywithcash for instructions and more information.

Check or Money Order. Taxpayers can send a check or money order with their tax return or when they get a bill. Before submitting a payment through the mail, taxpayers should consider one of the quick and easy electronic payment options.

Options for Taxpayers Who Can’t Pay Now The IRS offers payment alternatives if taxpayers can’t pay what they owe in full. A short-term payment plan may be an option. Taxpayers can ask for a short-term payment plan for up to 120 days. A user fee doesn’t apply to short-term payment plans.

Taxpayers can also ask for a longer term monthly payment plan or installment agreement. A $149 user fee applies to monthly payment plans or installment agreements that can be reduced to $31 if payments are made by direct debit.

Individual taxpayers who owe more than $50,000 and businesses that owe more than $25,000 must submit a financial statement with their request for a payment plan.

Another option may be an Offer in Compromise. An Offer in Compromise is an agreement between the taxpayer and the IRS to settle their tax debt for less than the full amount they owe. Not everyone qualifies for an offer. Taxpayers should use the Offer in Compromise Pre-Qualifier to decide if an offer in compromise is right for them.

Depending on the circumstances, a taxpayer may consider borrowing the tax amount due. The costs of getting a loan or even paying by credit card may be less than the penalties and interest accrued.

If taxpayers can’t find an option that works for them, the IRS may offer other alternatives, such as a temporary suspension of collection. Taxpayers should contact the IRS at 800-829-1040 or call the phone number on their bill or notice to discuss other options.

Now that tax time is over, here are three things you need to be doing to help your business…

1. Communicate

….with your CPA or Accountant

Review your tax return …he has time to go over the details with you now that his “crunch time” is over

Get the year-end adjusting journal entries and adjustments from him to update your QuickBooks or accounting software to keep your keep your books accurate…

Ask him to help or show you what things you can do to help his life easier at tax time…recording entries in the correct account might prevent all these journal entries in the first place…and you might learn a thing or two in the process!

Ask him any software questions you have …chances are he’s using the same software (QuickBooks, Wave, etc.) as you are

…with your Banker

Now is the time to bring a copy of your business return to him and discuss….if you ever have to borrow money, it’s good to have history with your banker… even if you’re not going to borrow money or open up another account right now, it’s always good to inquire about the rates and the borrowing process.

…with your Retirement Planner

If you don’t have one, get one! He can tell you the pros and cons of each type of plan and how your business can benefit by having one

2. Save

…taxes

by keeping better track of your business miles

Every hundred miles you drive, you can write off about $55 in mileage expense… keep a log in your vehicle or better yet, there’s an app for that! …every little bit helps and by the end of the year all those miles driven to the bank or supply store or to a customer add up to a nice deduction!

…money

to cover the tax bite at year end

By saving during the year, you avoid having to borrow money at tax time to pay your bill or even worse, paying penalties and interest if you don’t pay on time…

Even if you set up quarterly tax payments, you should put money aside to cover that chunk of money you have to pay to the feds or to the state…

If you open a savings or money market account instead of leaving it in a non-interest-bearing checking account, you might even make some extra money

…time

Did you ever wonder how nice it would be to get back or recover 5 to 20 hours per month of your time?

That saved time could be used to market your business and pick up new clients

By outsourcing your bookkeeping or payroll work, you open up more time for you to meet with prospective customers or meet with existing customers and offer them extra services

Your time is better spent increasing your revenue than doing admin work that someone else can probably do better, more accurately and faster…sure, you have to pay them but the cost of subcontracting out the bookkeeping is probably less than the revenue gained with a new customer.

3. Plan

…your business continuation

What would happen to your business if you became critically ill or called away due to a family member crisis?

What happens to your customers or clients if such a scenario would occur?… you’ve heard the old adage, “fail to plan, plan to fail”

Start creating a checklist of important resources and phone numbers… talk with someone you trust to take over your business temporarily or permanently if things go south

If you got a family and your business is your “retirement plan”, the loss of customers won’t make life easier for your loved ones

…for your next tax return

Sure, you just finished filing your tax return but now is the best time to plan for the current year return

How does the new tax law affect my business? What expenses should I cut back or increase due to the new tax law? Should I invest in new equipment or machinery for my business?

Talk with your CPA or tax preparer …go over the year-to-date numbers and set up a plan of action to take advantage of the tax law and avoid problems later on

…on making your business better and more efficient

Look into outsourcing your bookkeeping work so you can spend more quality time increasing your revenues

Get rid of old equipment that is killing your bottom line with repairs and high maintenance costs

Invest in modern technology that saves you and your employees time and frustration

Review processes within your organization that need to be updated and/or fine-tuned

Take a look at your personnel and make sure you’ve got the right person for every job or position in your company

Plan to make your life easier in this very complicated world…

Art Goudey, Jr., President and sole-owner of Compass Consulting Services, PA in Raleigh, NC. He is also a Certified QuickBooks® Pro Advisor, a member of the American Institute for Certified Public Accountants (AICPA), the North Carolina Association of CPA’s (NCACPA) and is a former chair of the NCACPA Technology Committee. art@compassconsulting.net